Meg says…

“Meg has a better, more realistic plan: spark job growth now by quickly enacting targeted tax cuts that are affordable and immediately impact key sectors of our economy to create new jobs.” p. 11

Meg Whitman 2010 Building a New California

But Meg…

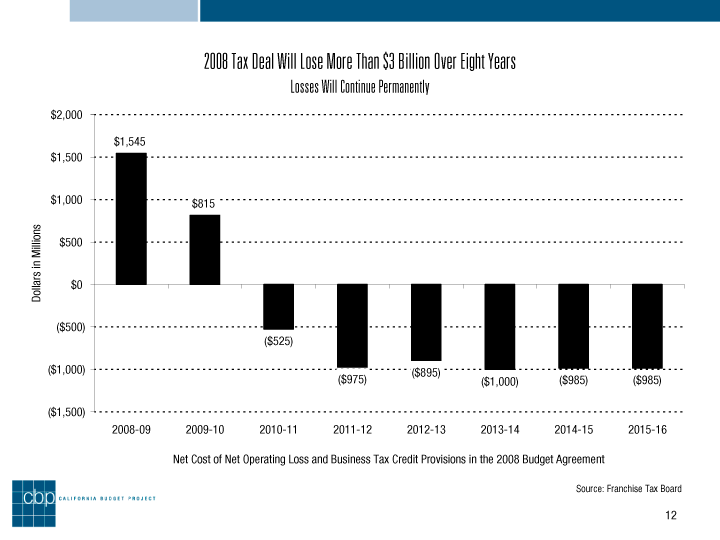

Your “targeted tax cuts” already exist. They are called Tax Expenditure Programs (TEPs). A brief history of TEPs is taken from the Legislative Analysts Office Report, Tax Expenditures and Revenue Options, April 7, 2008:

“Targeted tax cuts” or “TEPs’... the tax expenditure concept was developed in the late 1960’s. Soon thereafter, California appears to have been the first state to have explored the use of tax expenditure information in the budget process. For example: In 1971, the Legislature enacted Chapter 1762, which required the Department of Finance (DOF) to publish two general reports on the state’s use of TEPs....in the 1975-76 Governor’s Budget, the department provided the first estimates of the revenue loss from specific tax expenditures.”

Facts about Meg’s “targeted tax cuts” or TEPs

TEPs refer “to various special tax provisions that reduce the amount of revenues the ‘basic tax’ system would otherwise generate in order to provide: benefits to certain groups of taxpayers and/or incentives to encourage certain types of behavior and activities….

- California has several hundred TEPs with an estimated 2008-09 value of nearly $50 billion…

- The main types of TEPs involve tax exclusions, exemptions, deductions, credits, special filing statuses, and preferential tax rates…

- Because program funding does not have to be annually appropriated through the budget process, there is normally no limit or control over the amount of money spent…

- TEPs only require a majority vote to establish but a two-thirds vote to be scaled back or eliminated if found to be ineffective or cost inefficient. – just the opposite of direct expenditure programs.…

- TEPs often experience large “windfall benefits” from compensating individuals and businesses for actions they would undertake anyway…

http://www.lao.ca.gov/handouts/Econ/2008/Tax_Expend_04_07_08.pdf

California Budget Project, “California Tax System”, p. 12

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

Creating Jobs using Targeted Tax Cuts or (TEPs)

Meg Says…Eliminate the Small Business Start-up Tax

“Meg will eliminate the $800 fee that new business start-ups are currently required to pay in California. Entrepreneurs should not be penalized for launching a business venture. The LLC filing fee is nothing more than a tax on jobs. The state that put “start-up” into the national lexicon needs to repeal this tax.” p. 11

But Meg…

Elimination of $800 Minimum Franchise Tax (MFT) for New Corporations Is Unnecessary, Not Fiscally Prudent ($60 million revenue loss): Whitman proposes to eliminate the $800 limited liability company (LLC) filing fee that new corporations pay to incorporate as an LLC. Under current law, the MFT is already waived for a C Corporation’s first two years of existence. Many LLCs currently pay no additional taxes because they are set up as holding companies or take all of their profit in the form of executive compensation and therefore pay no corporation tax. The $800 tax, which has been in place since the 1987 federal tax reform conformity legislation, is a nominal and fair amount for the privilege of conducting business as an LLC in California.

Meg Says…Eliminate the Factory Tax

“California is only one of three states that taxes manufacturing equipment without offering a tax credit or exemption.” p. 11

But Meg…

Sales Tax Exemption or Tax Credit for Manufacturing Equipment Will Not Create New Jobs, Only Serve to Significantly Increase State Budget Deficit ($1-2 billion/yr. revenue loss): ... A sales tax exemption is preferred to a credit given the administrative nightmare of the now expired manufacturers’ investment tax credit (MIC) for both taxpayers and tax administrators. The MIC was enacted in 1994 with a promise by proponents that it would create 390,000 new jobs by 2004. The MIC expired at the end of 2003 because it failed to meet even a minimum threshold of 100,000 new manufacturing jobs that it needed to create to stay in effect. The truth of the matter is that U.S. manufacturing jobs are going overseas due to market conditions, not state and federal tax rates.”

Meg Says…Increase the Research and Development Tax Credit

“…increase the R & D tax credit for California businesses from 15 percent to 20 percent, which conforms to the federal level. This is the same level of tax credit that many of the states we compete with offer today. This tax cut will promote investment in the technologies and industries of the future.” p. 11

But Meg…

“There are more than $10 billion in unused state R & D credits being ‘carried over’ for future use. For taxpayers with large amounts of unused credits, current R & D decisions are unlikely to be affected by their ability to stockpile additional credits...California’s R & D credit rate is the third highest in the country.”

The Legislative Analysts Office (LAO), “Tax Expenditures and Revenue Options,” April7, 2008. p.10

http://www.lao.ca.gov/handouts/Econ/2008/Tax_Expend_04_07_08.pdf

And…

“California already has the most generous research and development credit in the country. It is so generous, relative to the amount of corporation tax, that many companies already zero out their entire tax liability. Adding more to that makes no economic sense. The September 2009 budget agreement permitted the sharing of these credits among affiliates, which means much more income can now be sheltered than ever before through use of the R & D tax credit. The state corporation tax is ¼ the federal rate, which is why state R & D tax credits are usually so much lower than the 20% federal rate....There has been no evidence presented that the current R & D rate is somehow ineffective in increasing R & D in California.”

http://www.kerstencommunications.com/miscellaneous/whitman-poizner-tax-plans-increase-state-budget-deficit-10-billion-provide-significant-tax-benefits-personal-fortunes-states-ultra-rich-taxpayers

Meg Says…Promote Investments for the Agriculture Industry

…by providing a tax credit to encourage investments in water-conservation technology, we can reduce our consumption and benefit all Californians”. p.11

But Meg…

Tax Credit for Water-Conservation Technology Would Not Increase Development of Such Technology, Only Serve to Widen State Budget Gap (Unknown Revenue Impact, Estimated at $10-20 million/year minimum): Investors will invest in water conservation technology if it makes economic sense to do so....The escalating prices of water, especially in Southern California, has created a growing market for this technology. It does not make sense for the state, at significant cost of lost revenues, to reward entrepreneurs for developing products for which there is a thriving market. The economic benefits of selling such devices is reward enough.”

http://www.kerstencommunications.com/miscellaneous/whitman-poizner-tax-plans-increase-state-budget-deficit-10-billion-provide-significant-tax-benefits-personal-fortunes-states-ultra-rich-taxpayers

No comments:

Post a Comment