“…California is one of a few states in the country that taxes capital gains at a higher rate than traditional income. This is double taxation at its worst. California’s tax treatment of capital gains is a major impediment to capital formation and investment in new jobs. We should align California tax treatment of capital gains with that of other competing states.” p. 11

But Meg…

“Not only does California tax capital gains at the same rate as any other income — not higher, as gubernatorial candidate Meg Whitman says — but it also is in the mainstream in its practice.”... of the 40 other states that levy an income tax, all but 10 essentially treat long-term capital gains the same as ordinary income — at least they did in 2007....”

In other words, California does what 30 other states do. By my reckoning, that makes it not "one of a few," but "right in the mainstream." Michael Hiltzik, “Whitman needs to get facts right on capital-gains tax,” Los Angeles Times.

http://www.latimes.com/business/la-fi-hiltzik-20100725,0,1228882.column

And...

“Over the past decade, state tax records show capital gains collections totaling $70.3 billion, ranging from a low of $3.2 billion annually to a high of $11.7 billion — an average of $7 billion between 2000 and 2009. The better the economy, the higher the collections as investors cash out their winnings.

Schwarzenegger’s budget estimates $5.3 billion in capital gains tax receipts in 2010.”

http://californiascapitol.com/blog/?p=2259

And...

“The argument that proponents of preferential treatment for capital gains make most frequently is that it is necessary to foster investment and to spur economic growth....The theory that reducing taxes on capital gains will lead to a more robust economy is nothing more than that – a theory. Rather, an array of experts – from impartial economists within the federal government to non-partisan analysts outside it – agrees on one central fact: there is little connection between lower capital gains taxes and higher economic growth, in either the short-run or the long-run

And...

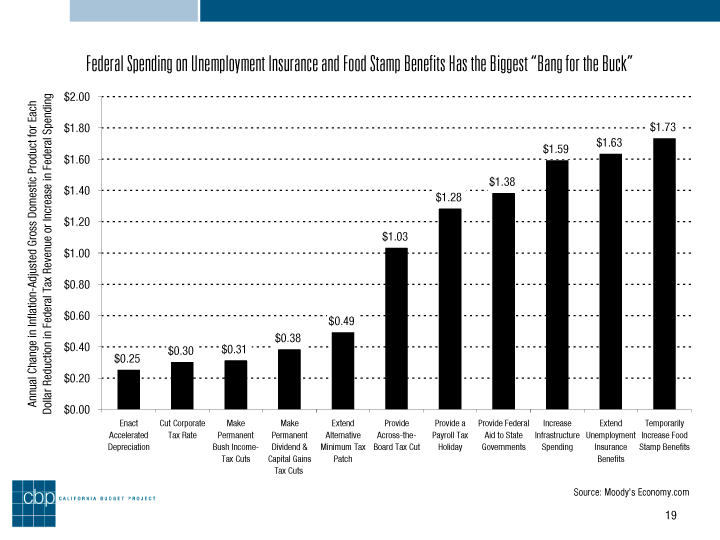

In 2002, the Congressional Budget Office (CBO) evaluated the stimulative effect that several different approaches to cutting taxes might have. It found that “capital gains tax cuts would provide little fiscal stimulus,” since most of the benefits of such cuts would accrue to high income households, households that are more likely to save than spend, when the very aim of such stimulus is to boost consumption. Indeed, the CBO determined that, of the range of approaches it examined, capital gains tax cuts were among the least effective. Similarly, but more recently, Mark Zandi, the Chief Economist of Moody’s economy.com, examined a set of proposals Congress could adopt to stimulate the economy in the wake of the credit crisis and the developing recession. He found that each dollar spent by the federal government in making President Bush’s dividend and capital gains tax cuts permanent would boost Gross Domestic Product (GDP) by just 38 cents. To put that in perspective, Zandi determined that each dollar dedicated to bolstering the food stamp program, extending Unemployment Insurance, or improving public infrastructure would yield over $1.50 in additional GDP.”

Zandi, Mark, Testimony before the US House of Representatives Committee on the Budget, January 27, 2009. (see “Bang for the Buck Chart” below)

And...

“...Len Burman, the Director of the joint Brookings Institution-Urban Institute Tax Policy Center, indicates that, over the last 50 years, real GDP growth has not varied in response to changes in capital gains tax rates; even when one accounts for the possible lag between a capital gains rate cut and subsequent economic activity, the relationship between rates and growth is not statistically significant.”

Burman, Leonard and Kravitz, Troy, “Capital Gains Tax Rates, Stock Markets, and Growth”, Tax Notes, November 7, 2005.

And...

“....Center for American Progress and the Economic Policy Institute reviews the impact that “supply-side” tax cuts, chief among which are lower rates for capital gains, have had on the US economy since 1981. It finds that such an approach to tax policy, when evaluated across a range of economic measures – such as the growth in Gross Domestic Product, median household incomes, average hourly earnings, or employment – simply does not work at the federal level.”

Ettlinger, Michael and Irons, John, Take a Walk on the Supply Side, Center for American Progress and Economic Policy Institute, Washington, DC, September 2008.

And...

“Attempting to use capital gains tax cuts to promote economic growth on a state-by-state basis is even more shortsighted, for at least two critical reasons. First, an unlimited capital gains tax cut is unlikely to benefit the local economy, since any new investment encouraged by that tax cut could occur anywhere in the United States – or abroad. Stated slightly differently, simply because Rhode Island offers a preferential tax rate for capital gains does not make it more likely that investors living in Rhode Island will steer capital towards companies based in the Ocean State and thus spur in-state economic activity. After all, they will receive the same tax cut whether they invest in companies based in Rhode Island, located on Long Island, or situated on Easter Island. Consequently, they will seek out the highest return on their investment, without regard to location, just as they would in the absence of a preferential rate for capital gains. Second, as noted earlier, a portion of any capital gains tax break will never find its way into the pockets of state residents nor, by extension, into the cash registers of local merchants or onto the balance sheets of local employers. This is due to the interaction between state and federal income taxes, with any reduction in state capital gains taxes partially offset by an increase in federal income tax liability.”

“To sum up, preferential treatment for capital gains is simply not an effective means of promoting economic growth…..”

Institute on Taxation and Economic Policy, “A Capital Idea: Repealing State Tax Capital Gains Would Ease Budget Woes and Improve Tax Fairness”. pp. 10-13.

www.itepnet.org/pdf/A_Capital_Idea.pdf

Finally...

As a CEO, Return on Investment (ROI) drove your Corporate decision making and spending However, as a candidate for Governor , who wants to govern California like a business, ROI appears to be irrelevant in your decision making process to cut taxes and government spending.

You advocate tax cuts that traditionally have an ROI of $0.25 to $0.50 for every dollar credit, while cutting spending on programs with an ROI from $1.28 to $1.73 for every dollar spent. An across the board tax cut, with an ROI of $1.03, is eliminated because it was too expensive.

Meg Says...“While making cuts in the marginal tax rates is a very important goal, at this moment we simply cannot afford a big, across-the-board tax cut that would irresponsibly grow the state’s oversized debt level and drop our bond rating to junk status” p. 11

California Budget Project’s, “California’s Tax System”, p 19

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

No comments:

Post a Comment