Monday, August 1, 2016

Friday, August 13, 2010

Targeted Tax Cuts aka Tax Expenditure Programs (TEPs)

UPDATE: Meg agreed to debate Jerry Brown, but the virtual debate will continue.

Meg says…

“Meg has a better, more realistic plan: spark job growth now by quickly enacting targeted tax cuts that are affordable and immediately impact key sectors of our economy to create new jobs.” p. 11

Meg Whitman 2010 Building a New California

But Meg…

Your “targeted tax cuts” already exist. They are called Tax Expenditure Programs (TEPs). A brief history of TEPs is taken from the Legislative Analysts Office Report, Tax Expenditures and Revenue Options, April 7, 2008:

“Targeted tax cuts” or “TEPs’... the tax expenditure concept was developed in the late 1960’s. Soon thereafter, California appears to have been the first state to have explored the use of tax expenditure information in the budget process. For example: In 1971, the Legislature enacted Chapter 1762, which required the Department of Finance (DOF) to publish two general reports on the state’s use of TEPs....in the 1975-76 Governor’s Budget, the department provided the first estimates of the revenue loss from specific tax expenditures.”

Facts about Meg’s “targeted tax cuts” or TEPs

TEPs refer “to various special tax provisions that reduce the amount of revenues the ‘basic tax’ system would otherwise generate in order to provide: benefits to certain groups of taxpayers and/or incentives to encourage certain types of behavior and activities….

http://www.lao.ca.gov/handouts/Econ/2008/Tax_Expend_04_07_08.pdf

California Budget Project, “California Tax System”, p. 12

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

Creating Jobs using Targeted Tax Cuts or (TEPs)

Meg Says…Eliminate the Small Business Start-up Tax

“Meg will eliminate the $800 fee that new business start-ups are currently required to pay in California. Entrepreneurs should not be penalized for launching a business venture. The LLC filing fee is nothing more than a tax on jobs. The state that put “start-up” into the national lexicon needs to repeal this tax.” p. 11

But Meg…

Elimination of $800 Minimum Franchise Tax (MFT) for New Corporations Is Unnecessary, Not Fiscally Prudent ($60 million revenue loss): Whitman proposes to eliminate the $800 limited liability company (LLC) filing fee that new corporations pay to incorporate as an LLC. Under current law, the MFT is already waived for a C Corporation’s first two years of existence. Many LLCs currently pay no additional taxes because they are set up as holding companies or take all of their profit in the form of executive compensation and therefore pay no corporation tax. The $800 tax, which has been in place since the 1987 federal tax reform conformity legislation, is a nominal and fair amount for the privilege of conducting business as an LLC in California.

Meg Says…Eliminate the Factory Tax

“California is only one of three states that taxes manufacturing equipment without offering a tax credit or exemption.” p. 11

But Meg…

Sales Tax Exemption or Tax Credit for Manufacturing Equipment Will Not Create New Jobs, Only Serve to Significantly Increase State Budget Deficit ($1-2 billion/yr. revenue loss): ... A sales tax exemption is preferred to a credit given the administrative nightmare of the now expired manufacturers’ investment tax credit (MIC) for both taxpayers and tax administrators. The MIC was enacted in 1994 with a promise by proponents that it would create 390,000 new jobs by 2004. The MIC expired at the end of 2003 because it failed to meet even a minimum threshold of 100,000 new manufacturing jobs that it needed to create to stay in effect. The truth of the matter is that U.S. manufacturing jobs are going overseas due to market conditions, not state and federal tax rates.”

Meg Says…Increase the Research and Development Tax Credit

“…increase the R & D tax credit for California businesses from 15 percent to 20 percent, which conforms to the federal level. This is the same level of tax credit that many of the states we compete with offer today. This tax cut will promote investment in the technologies and industries of the future.” p. 11

But Meg…

“There are more than $10 billion in unused state R & D credits being ‘carried over’ for future use. For taxpayers with large amounts of unused credits, current R & D decisions are unlikely to be affected by their ability to stockpile additional credits...California’s R & D credit rate is the third highest in the country.”

The Legislative Analysts Office (LAO), “Tax Expenditures and Revenue Options,” April7, 2008. p.10

http://www.lao.ca.gov/handouts/Econ/2008/Tax_Expend_04_07_08.pdf

And…

“California already has the most generous research and development credit in the country. It is so generous, relative to the amount of corporation tax, that many companies already zero out their entire tax liability. Adding more to that makes no economic sense. The September 2009 budget agreement permitted the sharing of these credits among affiliates, which means much more income can now be sheltered than ever before through use of the R & D tax credit. The state corporation tax is ¼ the federal rate, which is why state R & D tax credits are usually so much lower than the 20% federal rate....There has been no evidence presented that the current R & D rate is somehow ineffective in increasing R & D in California.”

http://www.kerstencommunications.com/miscellaneous/whitman-poizner-tax-plans-increase-state-budget-deficit-10-billion-provide-significant-tax-benefits-personal-fortunes-states-ultra-rich-taxpayers

Meg Says…Promote Investments for the Agriculture Industry

…by providing a tax credit to encourage investments in water-conservation technology, we can reduce our consumption and benefit all Californians”. p.11

But Meg…

Tax Credit for Water-Conservation Technology Would Not Increase Development of Such Technology, Only Serve to Widen State Budget Gap (Unknown Revenue Impact, Estimated at $10-20 million/year minimum): Investors will invest in water conservation technology if it makes economic sense to do so....The escalating prices of water, especially in Southern California, has created a growing market for this technology. It does not make sense for the state, at significant cost of lost revenues, to reward entrepreneurs for developing products for which there is a thriving market. The economic benefits of selling such devices is reward enough.”

http://www.kerstencommunications.com/miscellaneous/whitman-poizner-tax-plans-increase-state-budget-deficit-10-billion-provide-significant-tax-benefits-personal-fortunes-states-ultra-rich-taxpayers

Meg says…

“Meg has a better, more realistic plan: spark job growth now by quickly enacting targeted tax cuts that are affordable and immediately impact key sectors of our economy to create new jobs.” p. 11

Meg Whitman 2010 Building a New California

But Meg…

Your “targeted tax cuts” already exist. They are called Tax Expenditure Programs (TEPs). A brief history of TEPs is taken from the Legislative Analysts Office Report, Tax Expenditures and Revenue Options, April 7, 2008:

“Targeted tax cuts” or “TEPs’... the tax expenditure concept was developed in the late 1960’s. Soon thereafter, California appears to have been the first state to have explored the use of tax expenditure information in the budget process. For example: In 1971, the Legislature enacted Chapter 1762, which required the Department of Finance (DOF) to publish two general reports on the state’s use of TEPs....in the 1975-76 Governor’s Budget, the department provided the first estimates of the revenue loss from specific tax expenditures.”

Facts about Meg’s “targeted tax cuts” or TEPs

TEPs refer “to various special tax provisions that reduce the amount of revenues the ‘basic tax’ system would otherwise generate in order to provide: benefits to certain groups of taxpayers and/or incentives to encourage certain types of behavior and activities….

- California has several hundred TEPs with an estimated 2008-09 value of nearly $50 billion…

- The main types of TEPs involve tax exclusions, exemptions, deductions, credits, special filing statuses, and preferential tax rates…

- Because program funding does not have to be annually appropriated through the budget process, there is normally no limit or control over the amount of money spent…

- TEPs only require a majority vote to establish but a two-thirds vote to be scaled back or eliminated if found to be ineffective or cost inefficient. – just the opposite of direct expenditure programs.…

- TEPs often experience large “windfall benefits” from compensating individuals and businesses for actions they would undertake anyway…

http://www.lao.ca.gov/handouts/Econ/2008/Tax_Expend_04_07_08.pdf

California Budget Project, “California Tax System”, p. 12

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

Creating Jobs using Targeted Tax Cuts or (TEPs)

Meg Says…Eliminate the Small Business Start-up Tax

“Meg will eliminate the $800 fee that new business start-ups are currently required to pay in California. Entrepreneurs should not be penalized for launching a business venture. The LLC filing fee is nothing more than a tax on jobs. The state that put “start-up” into the national lexicon needs to repeal this tax.” p. 11

But Meg…

Elimination of $800 Minimum Franchise Tax (MFT) for New Corporations Is Unnecessary, Not Fiscally Prudent ($60 million revenue loss): Whitman proposes to eliminate the $800 limited liability company (LLC) filing fee that new corporations pay to incorporate as an LLC. Under current law, the MFT is already waived for a C Corporation’s first two years of existence. Many LLCs currently pay no additional taxes because they are set up as holding companies or take all of their profit in the form of executive compensation and therefore pay no corporation tax. The $800 tax, which has been in place since the 1987 federal tax reform conformity legislation, is a nominal and fair amount for the privilege of conducting business as an LLC in California.

Meg Says…Eliminate the Factory Tax

“California is only one of three states that taxes manufacturing equipment without offering a tax credit or exemption.” p. 11

But Meg…

Sales Tax Exemption or Tax Credit for Manufacturing Equipment Will Not Create New Jobs, Only Serve to Significantly Increase State Budget Deficit ($1-2 billion/yr. revenue loss): ... A sales tax exemption is preferred to a credit given the administrative nightmare of the now expired manufacturers’ investment tax credit (MIC) for both taxpayers and tax administrators. The MIC was enacted in 1994 with a promise by proponents that it would create 390,000 new jobs by 2004. The MIC expired at the end of 2003 because it failed to meet even a minimum threshold of 100,000 new manufacturing jobs that it needed to create to stay in effect. The truth of the matter is that U.S. manufacturing jobs are going overseas due to market conditions, not state and federal tax rates.”

Meg Says…Increase the Research and Development Tax Credit

“…increase the R & D tax credit for California businesses from 15 percent to 20 percent, which conforms to the federal level. This is the same level of tax credit that many of the states we compete with offer today. This tax cut will promote investment in the technologies and industries of the future.” p. 11

But Meg…

“There are more than $10 billion in unused state R & D credits being ‘carried over’ for future use. For taxpayers with large amounts of unused credits, current R & D decisions are unlikely to be affected by their ability to stockpile additional credits...California’s R & D credit rate is the third highest in the country.”

The Legislative Analysts Office (LAO), “Tax Expenditures and Revenue Options,” April7, 2008. p.10

http://www.lao.ca.gov/handouts/Econ/2008/Tax_Expend_04_07_08.pdf

And…

“California already has the most generous research and development credit in the country. It is so generous, relative to the amount of corporation tax, that many companies already zero out their entire tax liability. Adding more to that makes no economic sense. The September 2009 budget agreement permitted the sharing of these credits among affiliates, which means much more income can now be sheltered than ever before through use of the R & D tax credit. The state corporation tax is ¼ the federal rate, which is why state R & D tax credits are usually so much lower than the 20% federal rate....There has been no evidence presented that the current R & D rate is somehow ineffective in increasing R & D in California.”

http://www.kerstencommunications.com/miscellaneous/whitman-poizner-tax-plans-increase-state-budget-deficit-10-billion-provide-significant-tax-benefits-personal-fortunes-states-ultra-rich-taxpayers

Meg Says…Promote Investments for the Agriculture Industry

…by providing a tax credit to encourage investments in water-conservation technology, we can reduce our consumption and benefit all Californians”. p.11

But Meg…

Tax Credit for Water-Conservation Technology Would Not Increase Development of Such Technology, Only Serve to Widen State Budget Gap (Unknown Revenue Impact, Estimated at $10-20 million/year minimum): Investors will invest in water conservation technology if it makes economic sense to do so....The escalating prices of water, especially in Southern California, has created a growing market for this technology. It does not make sense for the state, at significant cost of lost revenues, to reward entrepreneurs for developing products for which there is a thriving market. The economic benefits of selling such devices is reward enough.”

http://www.kerstencommunications.com/miscellaneous/whitman-poizner-tax-plans-increase-state-budget-deficit-10-billion-provide-significant-tax-benefits-personal-fortunes-states-ultra-rich-taxpayers

Capital Gains Tax Cuts: Biggest "Bang for the Buck"? - Targeted Tax Cuts aka Tax Expenditure Programs (TEPs) (continued)

Meg Says...Eliminate the State Tax on Capital Gains

“…California is one of a few states in the country that taxes capital gains at a higher rate than traditional income. This is double taxation at its worst. California’s tax treatment of capital gains is a major impediment to capital formation and investment in new jobs. We should align California tax treatment of capital gains with that of other competing states.” p. 11

But Meg…

“Not only does California tax capital gains at the same rate as any other income — not higher, as gubernatorial candidate Meg Whitman says — but it also is in the mainstream in its practice.”... of the 40 other states that levy an income tax, all but 10 essentially treat long-term capital gains the same as ordinary income — at least they did in 2007....”

In other words, California does what 30 other states do. By my reckoning, that makes it not "one of a few," but "right in the mainstream." Michael Hiltzik, “Whitman needs to get facts right on capital-gains tax,” Los Angeles Times.

http://www.latimes.com/business/la-fi-hiltzik-20100725,0,1228882.column

And...

“Over the past decade, state tax records show capital gains collections totaling $70.3 billion, ranging from a low of $3.2 billion annually to a high of $11.7 billion — an average of $7 billion between 2000 and 2009. The better the economy, the higher the collections as investors cash out their winnings.

Schwarzenegger’s budget estimates $5.3 billion in capital gains tax receipts in 2010.”

http://californiascapitol.com/blog/?p=2259

And...

“The argument that proponents of preferential treatment for capital gains make most frequently is that it is necessary to foster investment and to spur economic growth....The theory that reducing taxes on capital gains will lead to a more robust economy is nothing more than that – a theory. Rather, an array of experts – from impartial economists within the federal government to non-partisan analysts outside it – agrees on one central fact: there is little connection between lower capital gains taxes and higher economic growth, in either the short-run or the long-run

And...

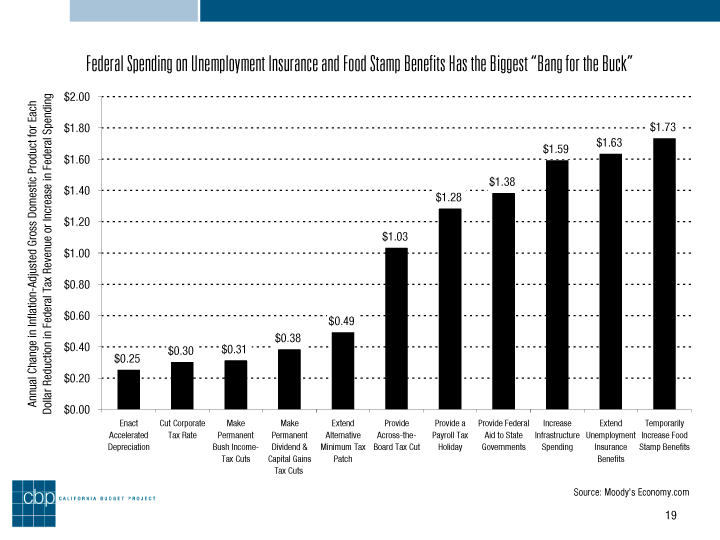

In 2002, the Congressional Budget Office (CBO) evaluated the stimulative effect that several different approaches to cutting taxes might have. It found that “capital gains tax cuts would provide little fiscal stimulus,” since most of the benefits of such cuts would accrue to high income households, households that are more likely to save than spend, when the very aim of such stimulus is to boost consumption. Indeed, the CBO determined that, of the range of approaches it examined, capital gains tax cuts were among the least effective. Similarly, but more recently, Mark Zandi, the Chief Economist of Moody’s economy.com, examined a set of proposals Congress could adopt to stimulate the economy in the wake of the credit crisis and the developing recession. He found that each dollar spent by the federal government in making President Bush’s dividend and capital gains tax cuts permanent would boost Gross Domestic Product (GDP) by just 38 cents. To put that in perspective, Zandi determined that each dollar dedicated to bolstering the food stamp program, extending Unemployment Insurance, or improving public infrastructure would yield over $1.50 in additional GDP.”

Zandi, Mark, Testimony before the US House of Representatives Committee on the Budget, January 27, 2009. (see “Bang for the Buck Chart” below)

And...

“...Len Burman, the Director of the joint Brookings Institution-Urban Institute Tax Policy Center, indicates that, over the last 50 years, real GDP growth has not varied in response to changes in capital gains tax rates; even when one accounts for the possible lag between a capital gains rate cut and subsequent economic activity, the relationship between rates and growth is not statistically significant.”

Burman, Leonard and Kravitz, Troy, “Capital Gains Tax Rates, Stock Markets, and Growth”, Tax Notes, November 7, 2005.

And...

“....Center for American Progress and the Economic Policy Institute reviews the impact that “supply-side” tax cuts, chief among which are lower rates for capital gains, have had on the US economy since 1981. It finds that such an approach to tax policy, when evaluated across a range of economic measures – such as the growth in Gross Domestic Product, median household incomes, average hourly earnings, or employment – simply does not work at the federal level.”

Ettlinger, Michael and Irons, John, Take a Walk on the Supply Side, Center for American Progress and Economic Policy Institute, Washington, DC, September 2008.

And...

“Attempting to use capital gains tax cuts to promote economic growth on a state-by-state basis is even more shortsighted, for at least two critical reasons. First, an unlimited capital gains tax cut is unlikely to benefit the local economy, since any new investment encouraged by that tax cut could occur anywhere in the United States – or abroad. Stated slightly differently, simply because Rhode Island offers a preferential tax rate for capital gains does not make it more likely that investors living in Rhode Island will steer capital towards companies based in the Ocean State and thus spur in-state economic activity. After all, they will receive the same tax cut whether they invest in companies based in Rhode Island, located on Long Island, or situated on Easter Island. Consequently, they will seek out the highest return on their investment, without regard to location, just as they would in the absence of a preferential rate for capital gains. Second, as noted earlier, a portion of any capital gains tax break will never find its way into the pockets of state residents nor, by extension, into the cash registers of local merchants or onto the balance sheets of local employers. This is due to the interaction between state and federal income taxes, with any reduction in state capital gains taxes partially offset by an increase in federal income tax liability.”

“To sum up, preferential treatment for capital gains is simply not an effective means of promoting economic growth…..”

Institute on Taxation and Economic Policy, “A Capital Idea: Repealing State Tax Capital Gains Would Ease Budget Woes and Improve Tax Fairness”. pp. 10-13.

www.itepnet.org/pdf/A_Capital_Idea.pdf

Finally...

As a CEO, Return on Investment (ROI) drove your Corporate decision making and spending However, as a candidate for Governor , who wants to govern California like a business, ROI appears to be irrelevant in your decision making process to cut taxes and government spending.

You advocate tax cuts that traditionally have an ROI of $0.25 to $0.50 for every dollar credit, while cutting spending on programs with an ROI from $1.28 to $1.73 for every dollar spent. An across the board tax cut, with an ROI of $1.03, is eliminated because it was too expensive.

Meg Says...“While making cuts in the marginal tax rates is a very important goal, at this moment we simply cannot afford a big, across-the-board tax cut that would irresponsibly grow the state’s oversized debt level and drop our bond rating to junk status” p. 11

California Budget Project’s, “California’s Tax System”, p 19

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

“…California is one of a few states in the country that taxes capital gains at a higher rate than traditional income. This is double taxation at its worst. California’s tax treatment of capital gains is a major impediment to capital formation and investment in new jobs. We should align California tax treatment of capital gains with that of other competing states.” p. 11

But Meg…

“Not only does California tax capital gains at the same rate as any other income — not higher, as gubernatorial candidate Meg Whitman says — but it also is in the mainstream in its practice.”... of the 40 other states that levy an income tax, all but 10 essentially treat long-term capital gains the same as ordinary income — at least they did in 2007....”

In other words, California does what 30 other states do. By my reckoning, that makes it not "one of a few," but "right in the mainstream." Michael Hiltzik, “Whitman needs to get facts right on capital-gains tax,” Los Angeles Times.

http://www.latimes.com/business/la-fi-hiltzik-20100725,0,1228882.column

And...

“Over the past decade, state tax records show capital gains collections totaling $70.3 billion, ranging from a low of $3.2 billion annually to a high of $11.7 billion — an average of $7 billion between 2000 and 2009. The better the economy, the higher the collections as investors cash out their winnings.

Schwarzenegger’s budget estimates $5.3 billion in capital gains tax receipts in 2010.”

http://californiascapitol.com/blog/?p=2259

And...

“The argument that proponents of preferential treatment for capital gains make most frequently is that it is necessary to foster investment and to spur economic growth....The theory that reducing taxes on capital gains will lead to a more robust economy is nothing more than that – a theory. Rather, an array of experts – from impartial economists within the federal government to non-partisan analysts outside it – agrees on one central fact: there is little connection between lower capital gains taxes and higher economic growth, in either the short-run or the long-run

And...

In 2002, the Congressional Budget Office (CBO) evaluated the stimulative effect that several different approaches to cutting taxes might have. It found that “capital gains tax cuts would provide little fiscal stimulus,” since most of the benefits of such cuts would accrue to high income households, households that are more likely to save than spend, when the very aim of such stimulus is to boost consumption. Indeed, the CBO determined that, of the range of approaches it examined, capital gains tax cuts were among the least effective. Similarly, but more recently, Mark Zandi, the Chief Economist of Moody’s economy.com, examined a set of proposals Congress could adopt to stimulate the economy in the wake of the credit crisis and the developing recession. He found that each dollar spent by the federal government in making President Bush’s dividend and capital gains tax cuts permanent would boost Gross Domestic Product (GDP) by just 38 cents. To put that in perspective, Zandi determined that each dollar dedicated to bolstering the food stamp program, extending Unemployment Insurance, or improving public infrastructure would yield over $1.50 in additional GDP.”

Zandi, Mark, Testimony before the US House of Representatives Committee on the Budget, January 27, 2009. (see “Bang for the Buck Chart” below)

And...

“...Len Burman, the Director of the joint Brookings Institution-Urban Institute Tax Policy Center, indicates that, over the last 50 years, real GDP growth has not varied in response to changes in capital gains tax rates; even when one accounts for the possible lag between a capital gains rate cut and subsequent economic activity, the relationship between rates and growth is not statistically significant.”

Burman, Leonard and Kravitz, Troy, “Capital Gains Tax Rates, Stock Markets, and Growth”, Tax Notes, November 7, 2005.

And...

“....Center for American Progress and the Economic Policy Institute reviews the impact that “supply-side” tax cuts, chief among which are lower rates for capital gains, have had on the US economy since 1981. It finds that such an approach to tax policy, when evaluated across a range of economic measures – such as the growth in Gross Domestic Product, median household incomes, average hourly earnings, or employment – simply does not work at the federal level.”

Ettlinger, Michael and Irons, John, Take a Walk on the Supply Side, Center for American Progress and Economic Policy Institute, Washington, DC, September 2008.

And...

“Attempting to use capital gains tax cuts to promote economic growth on a state-by-state basis is even more shortsighted, for at least two critical reasons. First, an unlimited capital gains tax cut is unlikely to benefit the local economy, since any new investment encouraged by that tax cut could occur anywhere in the United States – or abroad. Stated slightly differently, simply because Rhode Island offers a preferential tax rate for capital gains does not make it more likely that investors living in Rhode Island will steer capital towards companies based in the Ocean State and thus spur in-state economic activity. After all, they will receive the same tax cut whether they invest in companies based in Rhode Island, located on Long Island, or situated on Easter Island. Consequently, they will seek out the highest return on their investment, without regard to location, just as they would in the absence of a preferential rate for capital gains. Second, as noted earlier, a portion of any capital gains tax break will never find its way into the pockets of state residents nor, by extension, into the cash registers of local merchants or onto the balance sheets of local employers. This is due to the interaction between state and federal income taxes, with any reduction in state capital gains taxes partially offset by an increase in federal income tax liability.”

“To sum up, preferential treatment for capital gains is simply not an effective means of promoting economic growth…..”

Institute on Taxation and Economic Policy, “A Capital Idea: Repealing State Tax Capital Gains Would Ease Budget Woes and Improve Tax Fairness”. pp. 10-13.

www.itepnet.org/pdf/A_Capital_Idea.pdf

Finally...

As a CEO, Return on Investment (ROI) drove your Corporate decision making and spending However, as a candidate for Governor , who wants to govern California like a business, ROI appears to be irrelevant in your decision making process to cut taxes and government spending.

You advocate tax cuts that traditionally have an ROI of $0.25 to $0.50 for every dollar credit, while cutting spending on programs with an ROI from $1.28 to $1.73 for every dollar spent. An across the board tax cut, with an ROI of $1.03, is eliminated because it was too expensive.

Meg Says...“While making cuts in the marginal tax rates is a very important goal, at this moment we simply cannot afford a big, across-the-board tax cut that would irresponsibly grow the state’s oversized debt level and drop our bond rating to junk status” p. 11

California Budget Project’s, “California’s Tax System”, p 19

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

Historical Debt and Tax Cuts: A Final Word - Targeted Tax Cuts aka Tax Expenditure Programs (TEPs) (continued)

Meg Says…Establish Academic Enterprise Zones

“…take advantage of the academic excellence at our universities and create economic opportunity zones to encourage businesses to locate within a specified zone around these institutions. Tax incentives offered within these zones would be focused on hiring workers, promoting research and development, increasing access to state funds and loans and encouraging a close collaboration with the universities.” p. 12

But Meg…

Establishing Academic Enterprise Zones Near Universities Would Expand the State’s Already Inefficient and Wasteful Enterprise Zone (EZ) Program ($50 to $100 million/yr. annual revenue loss): The state’s current $300 million EZ program, which provides tax benefits in targeted zones throughout the state, is fraught with waste, fraud, and abuse as well documented by the California Budget Project and others (seeCalifornia’s Enterprise Zones Miss the Mark). Unfortunately, all reform attempts have failed in the Legislature thus far. Expanding a current program that is widely regarded as wasteful, inefficient, and loophole-ridden, is not a smart idea. Companies, largely specializing in R & D, are already congregated around the state’s premier university campuses. Most of these firms already take advantage of the state’s generous R & D tax credit. It makes no economic sense to reward these companies for locating in areas where it already makes economic sense for them to be located.

California Budget Project, “California’s Enterprise Zones Miss the Mark”

http://www.cbp.org/pdfs/2006/0604_ezreport.pdf

Meg Also Says...

“…the University of California, San Diego and the biotech region of San Diego are closely linked and provide leverage points for significant economic growth and job creation. The same is true in communities where other UC campuses are located.” p.12

But Meg...

“....why technology firms need new incentives to locate near Berkeley, Stanford, UC San Diego and UC Irvine, neighborhoods already bristling with them, isn't too clear.”

http://www.latimes.com/business/la-fi-hiltzik-20100725,0,1228882.column

Meg Says…Accelerate Depreciation of New Business Equipment

"…provide a more favorable depreciation schedule to encourage farmers, manufacturers and other companies to invest in new equipment and technology that will make them mire competitive and better able to hire Californians.” p. 12.

But Meg…

The effects of accelerated depreciation, or rapid amortization, under AB 1404 were evaluated by the Legislative Analyst’s Office in 1985 which found:

“In short, there is no empirical evidence indicating that AB 1404 has, in fact, had much of an effect on either the level of investment in cogeneration equipment or the level of economic activity generally. Rather, the available evidence suggests that the measure's primary effect has been simply to redistribute income between taxpayers, investors in cogeneration equipment, the state government, and the federal government…p. 27

In order for tax incentives such as shortened amortization periods to have significant positive economic effects, they must increase the level of investment in cogeneration equipment and facilities above what it would be otherwise. If they do not do so, the primary effect of these incentives is simply to redistribute income--to those investors who do not change their behavior but nevertheless qualify for the incentives, and to the federal government. These “windfall” benefits come at the expense of the State Treasury and California taxpayers who must directly or indirectly pay for them.” p. 25

Legislative Analyst's Office: “Cogeneration Equipment Investments: The Effects of Rapid Amortization”, 1985.

http://www.lao.ca.gov/reports/1985/476_0685_cogeneration_equipment_investments_the_effects_of_rapid_amortization.pdf

And...

“It is also possible for the government to provide too large an R & D incentive. If this happens, investment will be diverted from other more productive uses to relatively inefficient R & D activities. This could hurt overall economic performance.”…p.84

Franchise Tax Board, “California Income Tax Expenditures: Compendium of Individual Provisions”, updated December 2008.

http://www.ftb.ca.gov/aboutftb/taxExp08.pdf

Meg Says…Provide a $10,000 Tax Credit for Home Purchases

“To encourage homeownership and lessen the economic damage of last year’s mortgage crisis, Meg will provide a $10,000 tax credit to the buyers of new and existing homes. This will boost California’s real estate industry and improve the values of existing homes.” p. 12

But Meg…

“…Schwarzenegger signed AB 183 allowing first time homebuyers a tax credit equal to the lesser of 5 percent of a home’s purchase price or $10,000....The measure is an extension of a similar credit that expired last year....The credits are capped at $200 million – half for buyers of new homes, half for first time buyers of existing homes...

Whitman says she would provide the same thing but makes no mention of limiting it to first-time homebuyers.”

http://californiascapitol.com/blog/?p=2259

Meg Says…Provide a Tax Credit for Green Tech Job Creation

“…create incentives for employers to create green tech jobs by offsetting part of the cost of hiring new workers through a tax credit. These credits will apply only to permanent jobs directly involved in the development of alternative energy and other environmentally friendly technologies” p. 12

But Meg…

“…On March 24, Schwarzenegger signed into law SB 71 allowing the state to grant a sales tax exemption for manufacturing equipment purchased by so-called green technology companies.

The law defines green as cogeneration technology, energy conservation, solar, biomass, wind, geothermal, specified hydro-electric, or any other energy efficient technologies that reduce the use of fossil and nuclear fuels.” Also included, “advanced electric distributive generation technology and energy storage technology.”

The law requires the Legislature be notified when the total of the exemptions hits $100 million. No further exemptions can be granted without legislative approval.”

http://californiascapitol.com/blog/?p=2259

Meg Says…A Final Word: California’s Debt Crisis

“We can’t continue to use gimmicks to patch up the structural problems with the General Fund, while billions get added on top of the state’s debt”. pp. 12-13.

Meg 2010 Building A New California, p.13

But Meg….A Final Fact Check

There appears to be a direct correlation between California’s rising debt and increases in tax cuts.

Corporate Budget Project, “California’s Tax System” p.11

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

“…take advantage of the academic excellence at our universities and create economic opportunity zones to encourage businesses to locate within a specified zone around these institutions. Tax incentives offered within these zones would be focused on hiring workers, promoting research and development, increasing access to state funds and loans and encouraging a close collaboration with the universities.” p. 12

But Meg…

Establishing Academic Enterprise Zones Near Universities Would Expand the State’s Already Inefficient and Wasteful Enterprise Zone (EZ) Program ($50 to $100 million/yr. annual revenue loss): The state’s current $300 million EZ program, which provides tax benefits in targeted zones throughout the state, is fraught with waste, fraud, and abuse as well documented by the California Budget Project and others (seeCalifornia’s Enterprise Zones Miss the Mark). Unfortunately, all reform attempts have failed in the Legislature thus far. Expanding a current program that is widely regarded as wasteful, inefficient, and loophole-ridden, is not a smart idea. Companies, largely specializing in R & D, are already congregated around the state’s premier university campuses. Most of these firms already take advantage of the state’s generous R & D tax credit. It makes no economic sense to reward these companies for locating in areas where it already makes economic sense for them to be located.

California Budget Project, “California’s Enterprise Zones Miss the Mark”

http://www.cbp.org/pdfs/2006/0604_ezreport.pdf

Meg Also Says...

“…the University of California, San Diego and the biotech region of San Diego are closely linked and provide leverage points for significant economic growth and job creation. The same is true in communities where other UC campuses are located.” p.12

But Meg...

“....why technology firms need new incentives to locate near Berkeley, Stanford, UC San Diego and UC Irvine, neighborhoods already bristling with them, isn't too clear.”

http://www.latimes.com/business/la-fi-hiltzik-20100725,0,1228882.column

Meg Says…Accelerate Depreciation of New Business Equipment

"…provide a more favorable depreciation schedule to encourage farmers, manufacturers and other companies to invest in new equipment and technology that will make them mire competitive and better able to hire Californians.” p. 12.

But Meg…

The effects of accelerated depreciation, or rapid amortization, under AB 1404 were evaluated by the Legislative Analyst’s Office in 1985 which found:

“In short, there is no empirical evidence indicating that AB 1404 has, in fact, had much of an effect on either the level of investment in cogeneration equipment or the level of economic activity generally. Rather, the available evidence suggests that the measure's primary effect has been simply to redistribute income between taxpayers, investors in cogeneration equipment, the state government, and the federal government…p. 27

In order for tax incentives such as shortened amortization periods to have significant positive economic effects, they must increase the level of investment in cogeneration equipment and facilities above what it would be otherwise. If they do not do so, the primary effect of these incentives is simply to redistribute income--to those investors who do not change their behavior but nevertheless qualify for the incentives, and to the federal government. These “windfall” benefits come at the expense of the State Treasury and California taxpayers who must directly or indirectly pay for them.” p. 25

Legislative Analyst's Office: “Cogeneration Equipment Investments: The Effects of Rapid Amortization”, 1985.

http://www.lao.ca.gov/reports/1985/476_0685_cogeneration_equipment_investments_the_effects_of_rapid_amortization.pdf

And...

“It is also possible for the government to provide too large an R & D incentive. If this happens, investment will be diverted from other more productive uses to relatively inefficient R & D activities. This could hurt overall economic performance.”…p.84

Franchise Tax Board, “California Income Tax Expenditures: Compendium of Individual Provisions”, updated December 2008.

http://www.ftb.ca.gov/aboutftb/taxExp08.pdf

Meg Says…Provide a $10,000 Tax Credit for Home Purchases

“To encourage homeownership and lessen the economic damage of last year’s mortgage crisis, Meg will provide a $10,000 tax credit to the buyers of new and existing homes. This will boost California’s real estate industry and improve the values of existing homes.” p. 12

But Meg…

“…Schwarzenegger signed AB 183 allowing first time homebuyers a tax credit equal to the lesser of 5 percent of a home’s purchase price or $10,000....The measure is an extension of a similar credit that expired last year....The credits are capped at $200 million – half for buyers of new homes, half for first time buyers of existing homes...

Whitman says she would provide the same thing but makes no mention of limiting it to first-time homebuyers.”

http://californiascapitol.com/blog/?p=2259

Meg Says…Provide a Tax Credit for Green Tech Job Creation

“…create incentives for employers to create green tech jobs by offsetting part of the cost of hiring new workers through a tax credit. These credits will apply only to permanent jobs directly involved in the development of alternative energy and other environmentally friendly technologies” p. 12

But Meg…

“…On March 24, Schwarzenegger signed into law SB 71 allowing the state to grant a sales tax exemption for manufacturing equipment purchased by so-called green technology companies.

The law defines green as cogeneration technology, energy conservation, solar, biomass, wind, geothermal, specified hydro-electric, or any other energy efficient technologies that reduce the use of fossil and nuclear fuels.” Also included, “advanced electric distributive generation technology and energy storage technology.”

The law requires the Legislature be notified when the total of the exemptions hits $100 million. No further exemptions can be granted without legislative approval.”

http://californiascapitol.com/blog/?p=2259

Meg Says…A Final Word: California’s Debt Crisis

“We can’t continue to use gimmicks to patch up the structural problems with the General Fund, while billions get added on top of the state’s debt”. pp. 12-13.

Meg 2010 Building A New California, p.13

But Meg….A Final Fact Check

There appears to be a direct correlation between California’s rising debt and increases in tax cuts.

Corporate Budget Project, “California’s Tax System” p.11

http://www.cbp.org/pdfs/2009/0902_Californias_Tax_System.pdf

Friday, July 16, 2010

Conversations with Meg Whitman

Meg Says...

...Forbes, a must read for corporate decision makers, ranks California

But Meg...

In the May 6, 2010 issue of Forbes, columnist Bruce Bartlett in “Tax Cuts and ‘Starving the Beast’” questions the notion that reducing the revenues of the government with tax cuts reduces government size and spending. History indicates that the opposite is true.

- After the 1981 Reagan tax cuts, Federal outlays rose from 21.7% of GDP in 1980 to 23.5% in 1983, before falling back to 21.3% of GDP by the time he left office.

- In 1993, when

- In 2005 Arnold Kling, a free market economist admitted...”cutting taxes did not help to reduce the size of government.

- Bill Nikanen of the Cato Institute has argued that Starve the Beast actually increased spending and made deficits worse.

Meg Says....

...California has the 48th worst business tax climate in America

But Meg

...According to the Franchise Tax Board, the share of Corporate income paid in taxes has fallen by nearly half since 1981. As Corporate income rose, the share of that income paid in taxes has fallen by nearly 50% since 1981. . California

Meg Says...

...California

But Meg...

The Legislative Analyst’s Office (LAO), California ’s nonpartisian fiscal and policy advisor, disagrees with the Varshnay and Tootelian’s (professors at California State University , Sacramento

“The V&T’s principal conclusions are that the total annual economic cost of all regulations in California

The LAO commented that the V & T conclusions “contain a number of serious shortcomings that render its estimates of the annual economic costs of state regulations essentially useless.” Specifically...“The V&T’s finding that the cost of regulations on small businesses amounts to roughly $134,000 per firm annually is overstated. Even if the direct cost of regulations is disproportionately borne by small businesses, as assumed by V&T, dividing $493 billion by the number of small businesses (3.7 million) is inappropriate and results in an overstatement.”...

Meg Says...

...She grew eBay from a start-up with 30 workers to a global company with more than 15,000 employees and nearly $8 billion in revenue.” (p. 8)

But Meg...

At a time when eBay was headed by one of the few high-profile female CEOs in Silicon Valley, Meg Whitman, the share of the company's managers and top officials who were female declined to 30 percent in 2005, from 36 percent five years earlier, according to federal employment data....” (The Mercury News siliconvalley.com, 2/10/2010)

Subscribe to:

Posts (Atom)